The following article does not constitute financial advice. Please always consult a regulated financial advisor before taking investment decision. I am not qualified to tell you what investments are relevant to your personal situation.

This post is about my experience as an individual investor who started and keeps maintaining his own investment portfolio. I was able to generate recurring income over the last years, leveraging on simple principles and my professional experience. I realised that it takes much less time and effort than I initially imagined. Here is the story.

Few years ago, despite spending most of my days surrounded by successful professional investors, I realised I had never really started to take care of my own money. As I finally started my journey as an investor, I documented it via a previous blog (no longer online). This page is a digest of what I learnt and the principles I follow.

Before going forward, if you are serious about setting you investment portfolio, make a rather small investment to build up your knowledge with three books Tony Robbins’ Unshakable, Robert Kiyosaki’s Rich Dad Poor Dad and Ramit Sethi’s I Will teach you to be Rich.

Personal investment Principles

- Think long term

- Diversify

- Keep it simple

- Do your research

- Accept the truth

1. Think long term: making money over a short period of time and being systematically right about your assumptions is something that almost no professional fund managers is able to achieve. That means you need to accept that you will not be able as an investor to make systematically significant short-term positive returns. Having said that, over the long run, stock markets have an upward trend and compounded interest (from stocks dividends or bond coupons) will add-up to generate additional capital.

Consider that over the last 90 years, the American stock market annualised return, represented in our post by the S&P500, is above 9%. I am sure that strikes you as being much higher than any deposit that your bank can offer. The trick here is the timeframe: 90 years. Individual investors may be able to capture significant average return with much higher probabilities if they increase their time frame: contrary to your job, you can’t expect regular payout increase.

Another reason why I use long-term thinking is that I wish to benefit from global trends. Several leading Private Banks recommend to their wealthy clients to rely on global long-term trends as a compass for their investment. Let’s consider the Private Banking giant UBS, which is recommending to invest in companies linked to Automation and Robotics, Education services, Emerging Markets healthcare or Energy Efficiency. Don’t you think that these industries shall enjoy a significant growth cycle from where they are now? But can you say when? Would it be next year or in 10 years time? My personal answer is that I do not mind, as my ultimate conviction is that such industries will eventually go though a strong cycle. It does not matter which industries you actually have the highest convictions on. As for me, I believe automation will be a significant driver of growth and transformation, that is why I decided to invest in BOTZ US ETF. Solar energy is also a conviction play, that is why TAN US ETF is also part of my portfolio. Another long term strategy I use is to invest in emerging markets – see next paragraph.

Emerging markets – unlocking long term value

Before we start, let me highlight that there are actually two major risks you need to be aware before you invest in emerging market: companies (be it through stocks or bonds) present a higher level of risks, due to local regulation and domestic markets realities, second (and too often overlooked by investors) the currency may depreciate, which mean that although the asset value may appreciate, your actual investment return in your reference currently (let’s assume US dollar) may be negative. Having said that, I am a strong believer in Emerging Markets and they represent a significant part of my portfolio.

To reduce the transaction costs (see definition below) associated with such investment, a broad Emerging Markets tracker could be useful. A well known tracker is the Vanguard FTSE Emerging Market (VWO UP) that is a global Emerging Markets Equity benchmark. I’ve used this tracker in my portfolio.

Many investors are eyeing to Chinese onshore market, as one of the potentially most attractive Emerging Markets. I am a strong believer in Chinese economy over the long run due to the country’s transformation and the development of a middle class on a large scale. To access this market, one may use the tracker called China AMC CSI 300 (3188 HK). I use this tracker in my portfolio.

Investors may also overweight specific countries that they are confortable with or particularly knowledgeable about such as Russia or Vietnam (you can find trackers for most countries).

Another area of interest for Emerging Markets could be Fixed Income securities. Here it becomes even more important to consider the currency risk. I personally stick to bonds issued by Emerging Markets governments (so called Sovereign bonds). An investor interested in domestic currencies may look for the VanEck Vectors J.P. Morgan EM Local Currency Bond (EMLC UP) or if he would favor USD denominated ones, he could elect Vanguard Emerging Markets Government Bond ETF (VWOB UP) . I use the former.

Unless you have a specific knowledge about Emerging Markets, it may be quite a risky decision to put any money on this asset class. Make sure you are getting advice from qualified professional.

2. Diversify

After reading the previous section, you may imagine that my portfolio is a mix of Technology and Emerging Markets, concentrating a very high level of risk. That is why the second principle is probably the most important of all: diversify.

Asset Allocation may sound to many as a fancy word, but this is nothing more than splitting your investments into different buckets that serve different goals. To me, it is probably the single most important rule of the money management game. Additionally, building up a “safe” bucket shall be a priority and I encourage you keep adding to this bucket if and when you manage to make money on more risky investments.

Let’s bring to the table one of the world’s most respected investor, Ray Dalio, founder of the Hedge Fund Bridgewater. After decades of successful investment, even such a manager came up with the conclusions that it would close to impossible to predict market movements and decided to rethink his approach to investment. He looked for a way to build a portfolio that he would hold for the long term and that could do reasonably well across different economic cycles. The backbone of this work is diversification across different types of assets. By diversifying enough the portfolio, Dalio and his team believe that the All Weather approach is sustainable over the long run, to the extend that Dalio’s personal trust money is now allocated to such portfolio.

The below screenshots are directly from Bridgewater’s website (see sources section for the link). In the first one, you will see the different risk adjusted return of the different asset classes. What Dalio is trying to explain is that over the long run you do not give up returns by diversifying to asset classes that have lower historical return: you will be potentially able to extract more sustainable returns thanks to diversification.

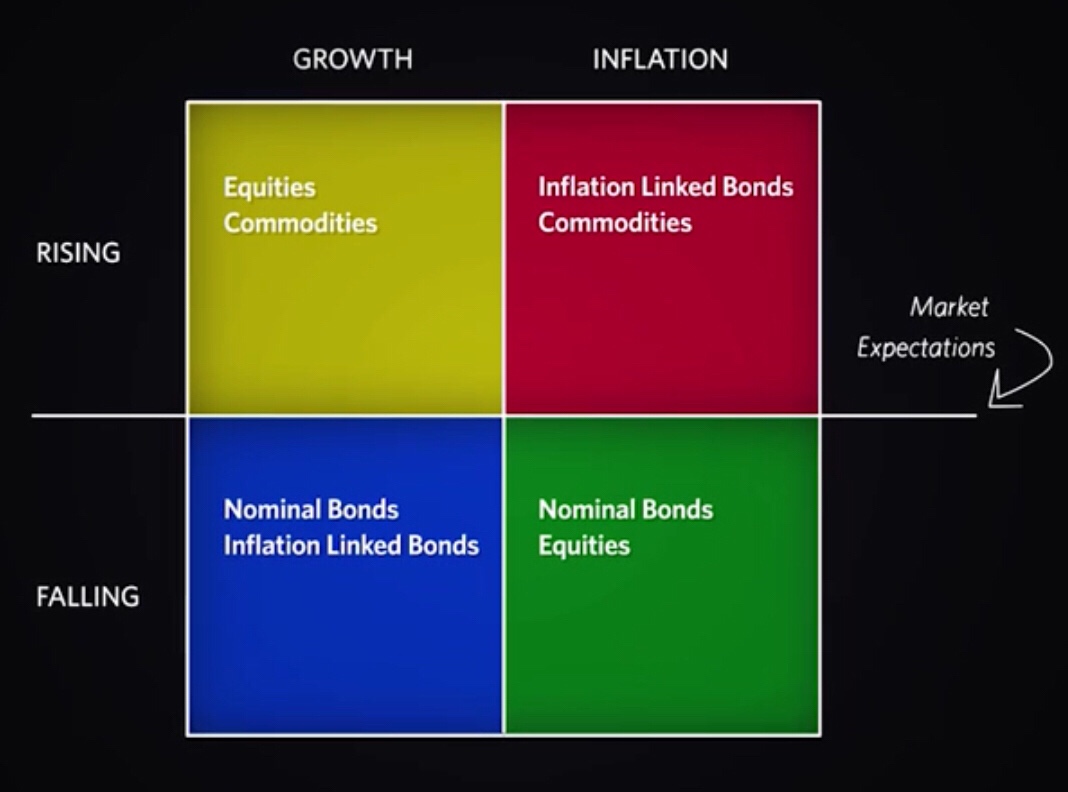

This second illustration is how Ray Dalio simplified the view of economic cycles and associated different asset classes to each scenario. This approach to economic cycles (and their two major drivers) helps to select asset classes that benefit historically from such scenarios. By putting them together, Bridgewater team anticipates to be always able to benefit from the ongoing economic scenario.

At this point in time you may wonder how you can invest in Bridgewater All Weather fund. Also it would be indeed an attractive idea to many, unless you are extremely wealthy, there is little chance that you will be able to join the hedge fund investors as the minimum ticket size is significantly high. Yet, you can indeed be inspired by Dalio’s work to build up a robust portfolio. By studying the All Weather fund I decided to add Inflation Linked Bonds to my own investment (both USA and Europe government bonds for me).

Can cryptocurrencies be part of a diversified investment portfolio? Cryptocurrencies such as Bitcoin and Etherium gained a lot of popularity with investors, especially since 2017. However, cryptocurrencies for now still have some high level of correlation with US stock market hence may bring less diversification to the table than anticipated.

3. Keep it simple

Unless you have a lot of time on your hands and a passion for the stock market, I believe it is best to keep your portfolio simple. I observe two rules:

- Whenever possible, prefer trackers to individual stocks

- Review the portfolio only quarterly (you may even prefer a longer timeframe)

The reason for preferring tracker is that it helps you to gain exposure to a significant number of equities or bonds via a single trade. It also prevents you from handling most of the Corporate Actions (administrative requirements when you are holding a stock, such a voting rights for new stock issuance). As for the number two, there are many fact-based evidence that support it, but my favourite story comes from a portfolio manager I met in 2014 and shared with me that over the last fours years, each year he would set-up in January an allocation strategy for the year and try to stick to it all year long. Yet, every year, due to market new or specific information, the portfolio manager ended up marginally changing the strategy, trying to capture short term profits. As he wanted to assess how much these deviations form the strategy was bringing to the return, he realised that they only ended-up in negative or minimal contribution, while most of the time increasing the risk position. If even a full time portfolio manager (with a successful track record) admits difficulty to capture long-term profit by ongoing marginal rebalancing, I consider than I would rather dedicate my personal time to other things than such adjustments to my own portfolio, that’s why the quarterly review works for me.

4. Do your research

There are everyday thousand of “hot” investments or “bargain” deal on the market. That’s a fact. Yet, as an individual, by the moment you are made aware of it, the real investment opportunity is probably gone, as professional investor already stepped in and pushed the price higher. That is why, regardless of whatever you read in the news or online, you need to spend time and get proper advice before pulling the trigger on an investment. I can not recommend enough that you look for a qualified professional advisor, that could save you a lot of money.

While doing your research, try to always understand “why” the opportunity is there. Also spend time looking at the fee element.

5. Accept the truth

I have lost money on some transactions and I will lose money on future ones. I bought some trackers too late (already went up) and bought expensive ETFs while similar cheaper one were available. When it comes to investments you can’t achieve perfection. It matters more to start early and to start somewhere, building your knowledge and experience in the process than actually waiting and waiting, reading countless books, looking for the Graal “ever-winning” strategy… All these delaying excuses are in fact the expression of our fear to fail. I had the same fear, despite working on a trading floor, I could not stand the idea of taking risk with my money. I was wrong and today I am grateful to my friends who mentored me through the first steps of setting-up my investment portfolio. Another consideration put me on the track: inflation over the long run erodes the value of your savings. In other words, cash tends to depreciate over the long run, hence the purchasing power you may end up with will be actually less than what it was when you initially saved the money.

If you have read the post until here, you probably know more than most people about starting an investment portfolio aiming at generate recurring income and wealth appreciation. Yet, I strongly recommend you keep building your knowledge on investment, primarily thanks to the books mentioned above but also take a look at this list of books that help me with money management and investments.

Taking action – the most important step

After I published an earlier version of this post, I got the following feedback from a friend “I read your post. I want to invest into ETFs. What shall I do now?” I would encourage you to take those steps:

- Find a licensed and registered financial advisors (it can be the wealth management arm of your commercial bank)

- Ask your usual commercial bank for their brokerage offer

- Compare the offer with a couple of flagship brokers available in your country

- If the prices are in the same price range, I would recommend that you start investing using your commercial bank’s offer. That is how I started and I decided to branch out when I increased my investment size and had more experience

- Work with the advisor to build a diversify portfolio – you can leverage for instance on the above content from Ray Dalio if that fits your situation

- Smart small – see the first trades as an investment in knowledge, as if you were paying for a course

- Take your time: research shows that investors prone to frequent rebalancing on average end up losing money. Be patient and set-up a quarterly of even less frequent review

- Don’t forget to build a SAFE bucket. No matter how smart you are and how much information you have, all asset classes are subject to significant market downturn.

–

Definitions

Transaction costs: the fees investors are charged, on top of the price of the asset, while buying and selling an asset. For instance, the fees that your broker may charge you when you buy a stock, or the rebalancing fee in your portfolio. These transactions are charged based on the number of transactions hence a simple way to limit them is actually to limit the number of orders (buy or sell) to a efficient minimum

Sources

S&P Returns over last 90 years: https://www.cnbc.com/2017/06/18/the-sp-500-has-already-met-its-average-return-for-a-full-year.html

UBS Global Long term investments https://www.ubs.com/global/en/wealth-management/chief-investment-office/key-topics/long-term-investments.html

Bridgewater All Weather fund https://www.bridgewater.com/research-library/the-all-weather-strategy/